How Much Can I Actually Afford

There is a difference between what a bank will approve you for and what you can actually afford. Those two numbers are often not the same and confusing them is one of the most common mistakes first time buyers make.

Start With Your Gross Income, Then Work Backward

Lenders typically use something called the 28/36 rule as a starting point. The idea is that your housing costs should not exceed 28 percent of your gross monthly income. And it should not exceed 36 percent of your total debt payments, including housing.

So if you bring in $6,000 a month before taxes, the 28 percent rule puts your maximum monthly housing payment around $1,680. That includes your mortgage principal, interest, property taxes, and homeowners insurance. If you are buying in an HOA community, add that in too.

What you are comfortable paying every month is a separate question.

What Actually Goes Into A Monthly Payment

A lot of buyers focus on the purchase price and forget that the monthly payment is made up of several things:

- Principal and interest (the loan itself)

- Property taxes

- Homeowners insurance

- PMI (Private Mortgage Insurance) if your down payment is under 20 percent

- HOA dues if applicable

A $300,000 home does not automatically mean a $1,500 payment. Depending on your interest rate, down payment, and local tax rates, that number could be anywhere from $1,600 to $2,200 or more. Running the real numbers before you start shopping matters.

Your Down Payment Changes Everything

Understanding what that choice costs you each month by how much you put down, your interest rate, and whether you pay a PMI affects your loan amount. A PMI typically runs between 0.5 to 1.5 percent of the loan per year and gets added to your monthly payment until you hit 20 percent equity. Putting 20 percent down eliminates PMI entirely, but is not required. Plenty of buyers put down 3 to 5 percent especially on their first home.

Don't Forget What Comes After The Closing

Your mortgage is not the only cost of owning a home. New buyers often get surprised by:

- Maintenance and repairs (a common rule of thumb is budgeting 1 percent of the home's value per year)

- Utility costs that are higher than renting

- Furniture and appliances if the home does not come with them

- Lawn care, pest control, and the small costs that add up

If your mortgage payment maxes out your budget, you are going to feel it the first time the water heater goes out.

What Lenders Look At Beyond Income

Your income is one piece of it. Lenders also look at:

- Your credit score (higher scores usually mean better interest rates)

- Your debt-to-income ratio, which accounts for car payments, student loans, and credit cards

- Your employment history

- How much cash you have left after the down payment and closing costs

Two buyers with the same income can get approved for very different amounts depending on what else is on their financial picture.

The Honest Answer

The number you can afford is the one that lets you cover your payment comfortably, keep an emergency fund, and still live your life. Not the maximum the bank will hand you.

A good starting point is to take your monthly take-home pay, subtract your existing monthly obligations, and see what is left. Your housing costs should be something you could handle even if something unexpected came up.

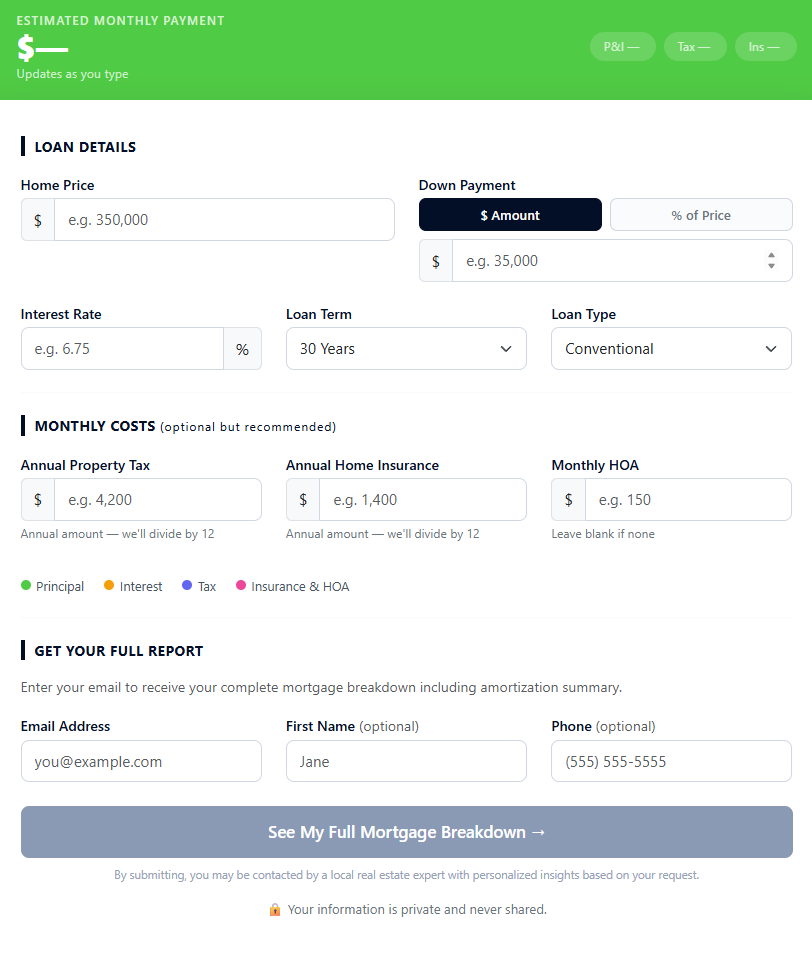

If you want to run actual numbers before you start talking to lenders, the ListSide Mortgage Calculator can help you test different purchase prices, down payments, and rates to see what payments look like in the real world.